|

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

July 29, 2009

Takeover Exemption by SEBI for Secur Industries Ltd.

INTRODUCTION

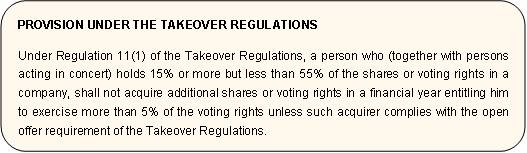

Securities and Exchange Board of India (“SEBI”) has by its order dated June 30, 2009, allowed an exemption to the promoters of Secur Industries Limited (“Target Company”) from complying with the mandatory open offer requirement under Regulations 11(1) of the SEBI (Substantial Acquisition of Shares and Takeovers) Regulations, 1997 (“Takeover Regulations”)1.

BACKGROUND & FACTS

Mr. H. P. Agarwal, the promoter of the Company, and certain persons acting in concert with him (“Acquirers”) were holding 7,13,207 equity shares in the Target Company constituting 17.49% of its paid up capital. As part of the transaction, the Acquirers proposed to acquire 1 million warrants (convertible into equity shares) and 1.2 million equity shares of the Target Company by way of preferential allotment, as a consequence of which the shareholding of the Acquirers in the Target Company would increase from 17.49% to 36.25% of the paid up capital, post preferential issue of equity shares and to 46.40% post conversion of warrants.

In view of this proposed transaction, the Acquirers had filed an application dated February 5, 2008, to SEBI under Regulation 3(1)(l) read with Regulation 4(2) seeking exemption from the applicability of Regulation 11(1) of the Takeover Regulations on the following grounds:

1. During the year 1993, the Target Company came out with a public issue but due to unfavorable market conditions, its business operations could not be continued. It was then that the Acquirers of the Target Company had infused funds to the tune of INR 12 million in the Target Company in order to aid the Target Company in times of its financial crisis. Thus the Target Company owes an unsecured loan of INR 12 million to the Acquirers. 2. The Target Company has been incurring substantial losses over numerous preceding financial years, due to which the net worth of the Target Company has been completely eroded and it is unable to pay off its debts. Moreover the Target Company is not in a position to raise funds from any outside source. 3. In order to improve the financial position of the Target Company and to enable it to meet the long term and short term working capital requirements, it was decided by the Target Company at its annual general meeting held in October 2007 to convert the unsecured loans into equity shares and to infuse further capital through the issuance of fresh warrants to the Acquirers. 4. Since the Acquirers are already in control of the Target Company, there will be no resultant change in control due to the proposed preferential allotment. Moreover the allotment shall be in due compliance with the Securities and Exchange Board of India (Disclosure and Investor Protection) Guidelines, 2000 (“DIP Guidelines”) and all other relevant provisions governing preferential allotment.

RECOMMENDATION OF THE TAKEOVER PANEL

Having regard to the poor performance and financial condition of the Target Company in the past financial years2, the Takeover Panel recommended that the Acquirers be granted exemption under Regulation 4 of the Takeover Regulations and be exempted from complying with the open offer requirement, since the proposed preferential allotment was not prejudicial to the interest of the Target Company or its public shareholders.

SEBI ORDER

After considering the submissions made on behalf the Acquirers and the recommendation of the Takeover Panel, SEBI noted that the proposed preferential allotment is required to improve the financial and working conditions of the Target Company and accordingly granted an exemption to the Acquirers from complying with the open offer requirement under Regulation 11(1) of the Takeover Regulations. The said exemption was made subject to the following two conditions:

1. the Target Company and the Acquirers should comply with the DIP Guidelines with regard to the proposed preferential allotment including the pricing norms, and 2. the proposed transaction shall be consummated within 15 days from the date of the SEBI order and relevant disclosures to be made by the Acquirers. CONCLUSION

SEBI has been granting exemptions from open offer under the Takeover Regulations if such exemption does not conflict with the interest of the target company or the public shareholders. There have been instances in the past where SEBI has rejected such exemption application, as in the case of Surya Pharmaceuticals 3, and has directed the acquirers to make an open offer.

However, in the current case, since the Target Company was not in a position to raise funds from any outside source and the proposed allotment to the Acquirers was being made with the sole purpose of bringing the company out of the financial crisis, Takeover Panel and SEBI has considered this to be a fit case for an exemption under Takeover Regulations.

“This decision of SEBI is commendable, but there could have been an alternative way to deal with warrants.” Says Mr. Kartik Ganapathy, Head of Corporate and Securities Team at Nishith Desai Associates. He added “While, it may have been imperative to exempt conversion of loans into equity from the open offer provisions taking into account the dismal financial position of the Company, one can argue that the interest of public shareholders could have been better served if the open offer was mandated at the time of conversion of warrants, thereby giving them an opportunity to exit.” .

_____________________________ 1 The said application was made by the Target Company on behalf of the promoter under Regulation 3(1) (l) read with Regulation 4(2) of the Takeover Regulations. 2 As per the balance sheet of the Target Company as on March 31, 2007, it has not recorded any sales for the past two years. Also the Target Company has not shown any fixed assets during the said period. 3 For further details please refer to our earlier hotline titled “SEBI denies takeover exemption to Futuristic Garments” dated June 26, 2009.

Harshita Srivastava, R. Vaidhyanadhan Iyer & Nishchal Joshipura

You may direct your comments to Ramya Krishnan-AniL +91 900465 0363 |

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|

|

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||