|

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

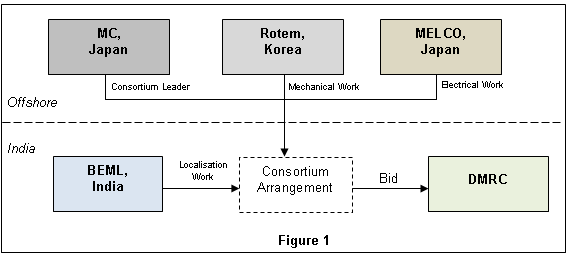

April 8, 2010 Unincorporated joint venture not held to be a taxable unit In the background of there being prolonged uncertainty and ambiguity on how unincorporated joint ventures and consortiums should be assessed under the Income Tax Act, 1961 (ITA), the Authority of Advance Rulings (AAR) has provided an instructive ruling in this regard in the case of M/s Hyundai Rotem Co., Korea and Anr. v/s DIT1. The ruling has provided the much sought guidance in terms of relevant factors that will ascertain the tax treatment of such entities and spelt out the circumstances when an unincorporated joint venture or a consortium should be treated as a separate taxable entity (i.e. association of persons (AoP)) under the provisions of the ITA. In the instant case the AAR, whilst resolving the query of whether a collaborative effort on the part of two or more parties which have formed a joint venture or a consortium to undertake contract works or other commercial activities could lead to an AoP, noted that in the absence of a specific definition of the term ‘AoP’, no ‘hard and fast rule or clear cut definition’ could be applied and stressed that such determination would be completely contingent on the relevant facts and circumstances of each case. Facts before the AAR For the purpose of bidding in a tender floated by and executing a project for Delhi Metro Rail Corporation (‘DMRC’), a consortium agreement was entered into between Mitsubishi Corporation, Japan (‘MC’), Hyundai Rotem Company, Korea (‘Rotem’), Mitsubishi Electric Corporation, Japan (‘MELCO’) and BEML ‘Limited, India (‘BEML’). The agreement provided for a ‘skill-set wise’ responsibility to each member and also appointed a consortium leader. Please refer to Figure 1 below for a diagrammatic representation Whilst dealing with the query, as put forth by the applicants MC and Rotem, on whether the consortium constituted an AoP, the AAR reverted to the meaning of the term “associate” which means “to join in common purpose, or to join in an action” as had been recognized by the Supreme Court in its landmark decision of CIT v. Indira Balakrishna. The AAR also referred its prior decisions on the point in the cases of GeoConsult ZT GmbH2 (on which the tax authorities relied upon to argue that an AoP was constituted) and Van Oord Acz BV3, on which the applicants relied to argue otherwise) and noted that a thorough analysis of the features of the entity, the work allocation, the arrangements and the agreements entered into and the facts and circumstances surrounding it, were essential in arriving at a conclusion as to the characterisation of an entity as an AoP. After analyzing the facts relevant to the applicant’s case and the contentions for and against the constitution of an AoP, the AAR ruled in the favour of the applicants and held that such a consortium arrangement would not constitute an AoP under the ITA for the following reasons: 1. The consortium agreement was entered into only for the purpose of participating in the tender and clearly stated that the parties did not intend to constitute a joint venture or a partnership; 2. Each consortium member would only share gross receipts, be responsible for its respective profits, losses and expenditures; 3. Segregation of work between the members based on their respective skill-set, such work not being capable of being assigned to or being supervised by another consortium member in case of default by one of the members; 4. Separate guarantee and undertakings were taken by the DMRC from the parent company of each consortium member for separate scope of work to be performed; Analysis It is interesting to note how the AAR has adopted a ‘features tests’ approach in arriving at an inference on the tax treatment of an unincorporated joint venture/ AoP, an undefined entity under the ITA. Further this ruling is likely to provide certainty and have an impact on industries involved in EPC (Engineering, Procurement and Construction), infrastructure, media, pharmaceutical, and similar sectors ,wherein similar arrangement are entered into. This ruling by the AAR will serve to provide a clarificatory basis to parties that form consortiums and unincorporated joint ventures solely for the purposes of participating into tenders for projects; and will serve as a guidance note which will assist such consortiums to structure their agreements and arrangements to obtain the desired tax treatment.

_________________

- Harshal Shah & Hanisha Amesur

You may direct your comments to Ramya Krishnan-AniL +91 900465 0363 |

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|

|

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||