|

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

April 27, 2010 Aggregation of contracts: Geographical and Commercial Coherence essential to constitute Permanent Establishment says Tribunal The Income Tax Appellate Tribunal (‘ITAT’) in a recent decision, in the case of Valentine Maritime (Mauritius) Ltd1 (‘Assessee’), laid down the elemental analysis to be carried out for determining the duration threshold limit by aggregation of contracts to constitute a permanent establishment (‘PE’) for foreign entities carrying out construction, engineering and supervisory works in India. The ITAT, while ruling in favour of the assessee over the question of aggregation of various contracts undertaken by the Assessee, pointed out that before aggregating contracts for calculating the threshold limit, the revenue must consider whether the activities carried out by such assessee are so inextricably interconnected that these cannot be viewed in isolation but only in conjunction to each other. Facts The Assessee, a Mauritius tax resident, engaged in business of marine and general engineering and construction, had executed 3 contracts in India (i) for charter of accommodation barge, (ii) for use of barge in domestic area; and (iii) for replacement of decks of which the first two were with the same client. The contracts being independent and not interconnected with each other, the Assessee claimed the income earned as business profits and sought to claim tax exemption on such income under the India-Mauritius tax treaty (India-Mauritius DTAA) on the grounds of non-existence of a PE. The main question before the ITAT, as was appealed by the revenue, was if the Assessee could be considered to have a PE in India by virtue of aggregation of the time periods of all 3 contracts which would cross the threshold as has been provided under the India-Mauritius DTAA. ITAT Analysis The ITAT, while deliberating on the question, highlighted points that are to be considered for the purpose of computing the threshold time limit, the gist of which is as follows:

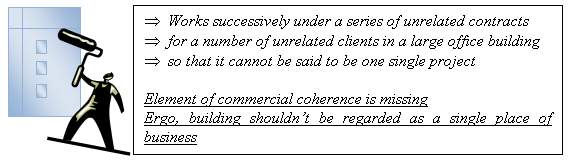

In this regard, the ITAT referred to the case of Sumitomo Corporation Vs DCIT wherein the theory of aggregating contracts on the ground of ‘mere commonality of the principal’ has been impliedly rejected if such contracts are independent and not capable of being coherent. The ITAT also touched upon the analysis provided in the OECD and UN Model Convention Commentaries which have expressed unanimity on the point that the duration test "applies to each individual site or project". The OECD says that while determining ‘coherence’, the question of geographical coherence precedes that of the commercial coherence. For geographical coherence, one really needs to determine whether different places of activities of an enterprise in the other contracting state are one place of business or different places of business. Only once the question of geographical coherence is answered in the positive, does the question of commercial coherence raised as to whether the work done constitutes one business venture or different business ventures On both the queries being answered in the positive, one can proceed to apply the contracts aggregation principal to determine the duration threshold. The ITAT, in the instant case, after applying the questions determined that the aggregation of contracts could not be applied, none of them being interconnected or interdependent, hence ruling in favor of the assessee. NDA Analysis This judgement most undoubtedly is essential for foreign enterprises involved in construction, engineering and supervisory works in India and in a manner provides relief to such foreign enterprises that undertake execution of multiple independent contracts. The OECD which is an advocate of the threshold test as stated above also does acknowledge the fact that this sort of an interpretation does leave scope of abuse by way of artificial contract splitting, each covering a period of less than threshold limit and each attributed to different company owned by the same group. A very popular example is that of a painter who is:

India, an observer of the OECD, has expressed reservation on the above, as in that geographical and commercial coherence are no prerequisites and even work carried out as the painter above would constitute a basic rule PE and includes discretion to include supervisory services and also negotiate the time threshold for creating a construction PE. It is heartening indeed however to note that the judicial bodies are applying its raison d'être and eliminating the uncertainty that results in its absence. ___________________

You may direct your comments to Ramya Krishnan-AniL +91 900465 0363 |

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|

|

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||