|

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

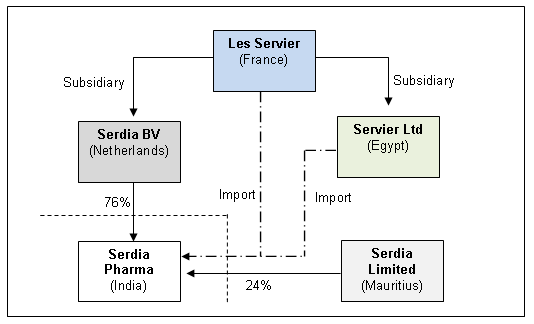

January 17, 2011 Importation of Active Pharmaceutical Ingredients under the transfer pricing radar In a recent transfer pricing ruling of the Mumbai Income Tax Appellate Tribunal1 which could have far reaching implications on pharmaceutical companies operating in India, it was held that the arm’s length price for importing active pharmaceutical ingredients (“API”) from related enterprises should be determined on the basis of price at which locally manufactured generic API are sold in the domestic market. Factual Background: Serdia Pharmaceuticals India Private Limited (“Serdia”) was a pharmaceutical company engaged in the business of producing drugs mainly in the field of cardiology and metabolic disorders. For the purpose of manufacturing these drugs, Serdia imported API from its related entities in France and Egypt (“International Transaction”). The issue faced by the Mumbai Income Tax Appellate Tribunal (“Tribunal”) was the determination of the correct arm’s length price (“ALP”) of these APIs imported into India. The two APIs under consideration were Trimetazidine and Indapamide which were imported at Rs 52,546 per kg and Rs 1,89,456 per kg respectively. Trimetazidine was the API which was used by Serdia for the manufacture of the finished dosage form (“FPF”) Flavedon 20, Flavedon Anti, being drugs used to treat anginal pain. On the other hand, Indapamide was used for the manufacture of FDF-Natrilix and Natrilix SR, being drugs that are used as a diuretic. Please find below a diagrammatical representation of the International Transaction, being the subject matter of dispute:

The tax payer had adopted ‘Transactional Net Margin Method’ (“TNMM”) for the purpose of determination of the correct arm’s length price of the API which was imported into India. The comparable companies, as selected by the tax payer, showed operating margins ranging between an operating loss of 13.29% to an operating profit of 19.07%. The arithmetic mean of margin of comparable companies was found to be 6.67% and since the operating profit of Serdia, being 8.76% on the net sales, was higher than that of its comparable competitors, the price of importing of the API was contended to be at an arm’s length price. On the other than, the Income Tax Department (“Revenue”) contended that the APIs purchased were at prices that were higher than that paid for similar APIs by other companies in India and that the Comparable Uncontrolled Price (“CUP”) was the most appropriate method. Please find below a table containing the price related information pertaining to the two API which were subject of dispute before the Tribunal:

On the basis of the information provided in the aforementioned table, the Revenue contended that the arm’s length price for Indapamide was Rs 40,375 per kg (not Rs.1,89,456 which was charged by the client) being the price paid for similar APIs manufactured by other companies in India. Likewise the arm’s length price was determined for importing Trimetazidine was 20,850 per kg (after making appropriate quality adjustments) and not Rs 52,546 per kg paid by Serdia. Judgment: The first point for consideration before the Tribunal was whether the Revenue was justified in failing to provide any defects in the method adopted by the tax payer and applying CUP method, being a method more appropriate compared to TNMM method, in the determination of the arm’s length price of the International Transaction. The Tribunal after analyzing the transfer pricing provisions relevant under Indian tax law held that the onus of selection of the “most appropriate method” for determining the arm’s length price of a transaction was on the tax payer. Since in the present case, the tax payer had failed to dispose this burden, the Revenue was justified in applying CUP Method without specifying the reasons for rejection of TNMM method. As regards the appropriateness of method, the Tribunal observed that, inspite of no hierarchy of methods being prescribed under Indian transfer pricing regulations, the traditional methods2 and particularly CUP method, was preferred as compared to other transaction profits methods.3 The reason for this preference was the greater reliability of the results obtained by applying these methods as compared to the transaction profits methods. Therefore the Tribunal concluded that whenever the CUP Method could be reasonably applied in determining the arm’s length price, this method should be followed. However the tax payer objected to the application of CUP Method on essentially two grounds. The first ground of objection was the difference in quality of Trimetazidine (API) imported by Serdia as compared to the locally produced API and consequential reduction in the efficacy of FDF produced using such APIs. In this regard, the tax payer submitted that GMP and HSE (Health, Safety and Environment) standards were followed pertaining to the API manufactured by Serdia’s related entities, thus ensuring a better quality. The Tribunal rejected this submission by holding that the high quality standards employed in manufacturing process conferred merely a certain degree of comfort pertaining to the minimum level of impurities but did not affect its comparability with the same API manufactured by generic drug companies. The second ground of objection, was the API manufactured by the Serdia were patent protected and therefore could not be compared to the generic API manufactured locally. However, the Tribunal observed that since the patent linked to these API had expired, an appropriate comparison could be made. In light of these obversations, the Tribunal held that the CUP Method and the arm’s length price for Indapamide was Rs 40,375 per kg and for importing Trimetazidine were 20,850 per kg. Analysis: It is a general principle of Indian jurisprudence that decisions of foreign courts and tribunals are not binding upon the Indian judicial and quasi-judicial bodies. Inspite of its mere persuasive value, foreign judgments have been increasingly relied upon by the Indian judiciary. In the present ruling, the Tribunal analyzed in detail, the Federal Court of Appeals’ ruling of Glaxosmithkline v. Her Majesty the Queen4 whose facts were similar to the case at hand. The Tribunal observed that the Federal Court had determined the matter in the favour of the assessee, on the basis of compulsions of the license agreement, because of which the tax payer was under an obligation to purchase the API at a higher price. Since in the present case, Serdia did not have any similar compulsion, the Tribunal was not inclined to rule in favour of the Serdia. In the light of the aforementioned observations of the Tribunal, maintaining of proper documentation pertaining to the importation of the API including incorporation of the commercial understanding into the licensing agreements between 2 related parties becomes critical. Further, the various adverse findings made against the tax payer due to the inconsistent statements made by it before the customs authorities on one hand and the transfer pricing officer on the other, reinforces the importance of consistent approaches being taken while representing one’s case before different wings of the tax authorities. The ruling, by comparing APIs imported into India with locally manufactured generic API has failed to appreciate the various costs which are involved in the importation of these ingredients, such as customs, freight, storage costs, etc. Further with this ruling, the onus of proving the appropriateness of the method has shifted onto the tax payer. Therefore the need of ensuring the appropriateness of the correct transfer pricing method becomes imperative pertaining to any international transaction entered into by any Indian entity with its associate entity.

__________________ 1 Serdia Pharmaceuticals (India) Private Limited v. ACIT, ITA Nos: 2469/ Mum/ 07 and 2531/ Mum/ 08 2 There are 3 methods which are considered to be traditional methods, being (a) comparable uncontrolled price method, (b) resale price method and (c) cost plus method 3 There are two methods which are considered as transaction profits methods; (a) profit split method and (b) transactional net margin method 4 2010 FCA 201

- Harshal Shah & Dr. Milind Antani You can direct your queries or comments to the authors

|

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|

|

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||