|

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

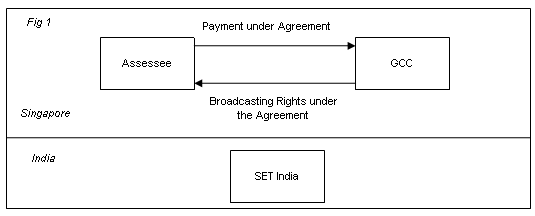

July 30, 2010 India-Singapore Treaty: Royalty Payments not Taxable in India Sans Economic Nexus with Permanent Establishment In a recent case of SET Satellite Singapore Pte Ltd.1 the Income Tax Appellate Tribunal, Mumbai (“ITAT”) has held that royalty payments made by a resident of Singapore to another Singaporean entity, as consideration of rights to transmit and broadcast matches etc. in India, are not subject to Indian withholding tax requirements. The ITAT in this case relied on Article 12(7) of the India-Singapore Tax Treaty (“Treaty”), which provides that royalty payments will be considered to arise in India, only if the royalty is paid by a resident of India or incurred in connection with its permanent establishment (“PE”) in India and such royalty is borne by such PE. Facts and Background MSM Satellite (Singapore) Pte. Ltd. (“Assessee”), a resident of Singapore, entered into an agreement (“Agreement”) with Global Cricket Corp Pte Ltd. (“GCC”), Singapore wherein in consideration for certain payments made by the Assessee, GCC granted the right to the Assessee to inter alia transmit, broadcast, exhibit visual or audio visual representations and/ or images of cricket matches, players etc. by any means of media in India, Pakistan, Bangladesh, Sri Lanka, Singapore and Malaysia.

In connection with the payments made to GCC under the said Agreement, the Additional Director of Income Tax (“ADIT”) contended that since the payments under the Agreement were in the nature of royalty payments under the Income Tax Act, 1961 (“ITA”), the Assessee should have deducted tax at source before making the payments to GCC. Since the Assessee failed to do so, the ADIT initiated proceedings against the Assessee. The ADIT does not seem to have gone into the provisions of the Treaty. Contrary to the observations of the ADIT, the Commissioner of Income Tax, Appeals (“CIT,A”) analyzed the provisions of the Treaty and held that even if the payments constituted royalty payments under the Treaty, the royalty payments did not arise in India within the meaning of the Treaty because there was no direct nexus with the activities of the PE of the Assessee in India. Thus, the CIT,A held that the Assessee was not liable to deduct tax at source from the payments made to GCC. Aggrieved by the order of the CIT,A, the tax department appealed to the ITAT. The Ruling The ITAT in its ruling has observed that in order for a royalty payment to arise in India in accordance with the Treaty, the royalty payment should be made by a person resident in India. Further, the royalty should be incurred in connection with and is borne by the PE of the payor in India. In the context of the case, the ITAT noted that the payor in this case, i.e. the Assessee, was not a resident in India. The tax department contended that SET India Private Ltd. (“SET India”) which undertook marketing activity for the Assessee in India was its PE in India. Hence, the payments received by SET India from the subscribers were indirectly the income derived by the Assessee. However, ITAT rejected this contention by observing that in order for royalty payments to arise in India, there should be an economic link between the liability for payment of such royalty and the PE. The economic link was missing in the Assessee’s case since the payments to GCC were liable to be paid by the Assessee’s head office in Singapore and not by SET India. Therefore, the Assessee was not liable to deduct tax at source. Analysis This ruling is of significant importance as it reaffirms the relevance of nexus in the context of the Treaty. As is seen in an increasing number of cases, the tax authorities have been trying to tax transactions between non-residents in India. With this ruling the ITAT has confirmed that in order for royalty payments to be taxable in India, there needs to be an economic nexus between the royalty payments and the PE in India. Without this linkage, such payments between two non-residents cannot be subjected to withholding tax requirements in India. The mere existence of PE is not sufficient for royalty to be chargeable to tax in India. It may be noted that provisions with respect to royalty payments are not similar in all tax treaties that India has signed. For example in the ruling given by the Authority for Advance Rulings2, where the question was whether royalty payments arise in India in the context of the India-US Tax Treaty, it was held that royalty is deemed to arise in India if the royalty relates to the use of, or the right to use, the property which gives rise to the royalty in India. Accordingly, where royalty payments are made between two non-residents, it is important to analyze the provisions of the relevant tax treaty to determine if royalty payments arise in India as this may not always be the case.

_____________________ 1 ITA No.7349/Mum/2004 2 Advance Ruling P. No. 22 of 1996 (238 ITR 99 AAR)

- Vivaik Sharma & Radhika Iyer

You may direct your comments to Ramya Krishnan-AniL +91 900465 0363

|

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|

|

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||