|

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

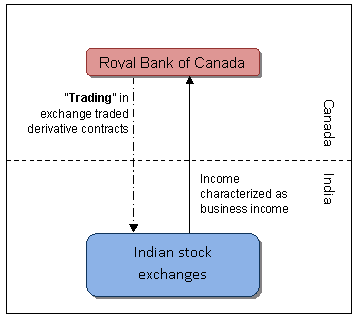

March 25, 2010 FIIs: Not taxable in absence of permanent establishment Ghost of Fidelity VII alive and kicking? The debate over characterization of income of Foreign Institutional Investors (“FIIs”) in India has been going on since some time now. This issue as to whether a FIIs income is business income or capital gains, came up, yet again, before the Authority for Advance Ruling (“Authority”) in case of Royal Bank of Canada1. The questions posed to the Authority by the Royal Bank of Canada related to taxability of income from futures and options contracts on one hand and that from purchase / sale of equity shares or other securities, on the other hand. In connection with income from derivatives, the Authority held, in line with In Re, Morgan Stanley and Co. International Limited2, that income derived by a foreign institutional investor (“FIIs”) from trading in exchange traded derivative contracts shall be in the nature of business income. Such business income would not subject to any tax in India, as long as the FII does not have a permanent establishment in India in accordance with the provisions of India-Canada Tax Treaty (“Treaty”). The Authority did not rule in relation with income from purchase / sale of equity shares or other securities.

Background The Royal Bank of Canada (the “Applicant”), registered as an FII with the Securities and Exchange Board of India (“SEBI”), undertakes trading in the derivatives segment of the Indian stock exchanges and intends to trade in equity instruments in near future. The Applicant approached the Authority to ascertain its tax liability with respect to the income earned from the derivative transactions and dealings in shares and securities undertaken in accordance with the provisions of the Income Tax Act, 1961 (the “Act”) and the India-Canada Tax Treaty. Arguments The Applicant primarily contended that the derivative transactions undertaken were a part of its trading activity with no intention to hold on long term basis and thus the income from such activity was in the nature of business income; not being taxable in India on account of the Applicant not having a permanent establishment in India in accordance with Article 7 of the India-Canada Tax Treaty. The Applicant placed heavy reliance on the case of In Re, Morgan Stanley and Co. International Limited (cited supra) where the Authority had upheld a similar argument in relation to derivative contracts. Similarly, the Applicant stated that the sale / purchase of shares and other securities was also for the purpose of earning trading profits. The Revenue, on the other hand, argued that as per the foreign exchange regulations and SEBI regulations, the Applicant being a FII, was only permitted to make ‘investments’ in capital markets and was not permitted to “trade” in shares, securities and derivative contracts. The Revenue further contended that provisions relating to taxation of FIIs under the Act (Section 115AD) did not envisage an FII to earn any income other than capital gains on account of transfer of securities. Ruling The Authority undertook detailed and in-depth analysis of the exchange control and SEBI regulations with respect to FIIs in India, the provisions of Section 115 AD of the Act and the rulings in this regard. They placed reliance on the ruling in Morgan Stanley where the Authority had observed that derivatives had a short life of 3 months and they do not yield any income in the nature of dividends; income can be derived only on their purchases and sales, and so they are held only as stock-in-trade. The Authority distinguished the ruling in Fidelity NorthStar Fund, relied upon by the Revenue, as the income therein did not relate to derivatives. However, the Authority referred to the observations in the ruling to the effect that there is no prohibition for FIIs to deal in exchange traded derivatives. As regards Section 115 AD of the Act, the Authority rejected the arguments of the Revenue and observed that Section 115AD had a wide scope of application and would include in its purview the trading income derived by FIIs from trading in exchange traded derivatives. Analysis The question relating to the characterization of income derived by FIIs has always been shrouded in confusion. While the Revenue has harped on the ineligibility of the FIIs to ‘trade’ in shares, securities and derivatives in accordance with the applicable laws, including that the Act does not envisage ‘trading’ activities being undertaken by an FII, the Authority had even previously ruled in Morgan Stanley and Fidelity Advisor Series VII3 that income derived from trade in shares and securities on account of the enormity and frequency of purchases and sales may be correctly characterized as business income. However, when faced with the same question in Fidelity NorthStar Fund, the Authority took a different stand and held that trading in shares and securities was not permitted under the applicable regulations, though they did observe that the regulations permitted trading in exchange traded derivative contracts. While this ruling is favorable for the FIIs with respect to income from exchange traded derivatives, the lack of clarity on the point of income from dealing in shares continues to trouble the industry. Further, the issue of offshore derivative instruments, where the underlying security may be an Indian capital asset, yet needs to see the face of the courts. Where on one hand, the government is going all the way to attract foreign investment in all forms, the uncertainty involving taxability of income of FIIs dealing with shares may hinder the process, especially so in times of great confusion in the Indian tax regime applicable to non-residents. _______________ 1 AAR No. 816/2009 2 [2005] 272 ITR 416 (AAR) 3 [2004] 271 ITR 1 (AAR)

- Neha Sinha & Mansi Seth

You may direct your comments to Ramya Krishnan-AniL +91 900465 0363 |

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|

|

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||