|

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

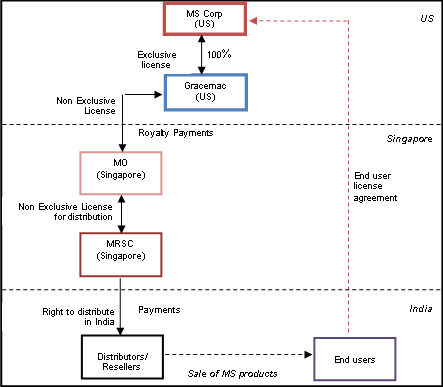

November 12, 2010 Payment for off-the-shelf software treated as royalty The debate relating to the issue of characterization of payments made for off-the-shelf has resurfaced again with the Delhi Income Tax Appellate Tribunal (“Tribunal”) holding that consumers are granted a license to use the software and therefore payments made in lieu thereof is in the nature of ‘royalty’ liable to tax under the India Income Tax Act, 1961 (“ITA”) and the India-USA Tax Treaty (“Tax Treaty”). Brief Facts Microsoft Corporation, Importantly, all the intellectual property in MS products vested with MS Corp and the end-users signed an End-User License Agreement (“EULA”) with MS Corp, which laid down the terms of use of the MS product.

Ruling In light of the terms of the EULA

and the restrictions upon the end-users for use of MS products, the Tribunal

held that the transaction in question was essentially a license of the MS

products and not an outright sale as claimed by the Appellants. Further, the

Tribunal rejected the difference between a ‘copyright’ and a ‘copyrighted

article’, and distinguished the rulings in Motorola Inc. v. DCIT1 and Tata Consultancy

Services v. State of Andhra Pradesh2 which While deliberating upon the merits of the case, the Tribunal categorically held that characterization of the payments made for computer software should solely be in accordance with the provisions of the ITA and the Tax Treaty. Further, the Tribunal declined to place reliance upon the OECD Commentary and the US IRS Regulations on the ground that the definition of ‘royalty’ and taxation thereof was precisely discussed in the ITA and in the absence of any ambiguity there was no necessity to refer to any external aids of interpretation.4 The Tribunal also held that the royalty payments received by Gracemac was liable to tax in India in accordance with Explanation to Section 9 of ITA which provides that royalty income of a non-resident shall be deemed to accrue or arise in India irrespective of whether the non-resident has a residence or a place of business or business connection in India. Besides the characterization issue, the Tribunal made some surprising observations with respect to the principles of treaty override. The Tribunal observed that in the event of a conflict between the provisions of domestic law and tax treaty, the domestic law provisions would override the treaty provisions. The Tribunal also imported ‘later-in-time doctrine’ stating that an amendment to domestic law after the treaty coming in force would override the provisions of the treaty. Analysis In this case, the Tribunal failed to ascertain the real nature of the transaction in question, which is surprising as both the Mumbai Tribunal5 and the Bangalore Tribunal6 have in recent rulings appreciated the difference between a ‘copyright’ and a ‘copyrighted article’ and have held that supply of off-the-shelf software is essentially the sale of a product as opposed to a license. Importantly on the question relating to attribution of royalty payments to Gracemac and taxation thereof in India, the Tribunal has completely dismissed the provisions of Article 12(7) of the Tax Treaty which would provide that in the absence of MSRC having a permanent establishment in India the royalty payable to Gracemac should not deemed to arise in India. This principle was recently upheld by the Mumbai Tribunal in SET Satellite Singapore Pte Ltd. v. ADIT7 in the context of the India-Singapore Tax Treaty, which is similarly worded as the India-US Tax Treaty. It is also pertinent to note that the Tribunal has made certain observations on important aspects of international law principles such as unilateral treaty override, which go against the core principles laid down in the ITA which specifically provide that a taxpayer is permitted to apply the provisions of the ITA or a tax treaty, whichever is more beneficial. This especially attains importance in light of the discussions surrounding the proposed Direct Taxes Code and issues relating treaty override which has been incorporated therein, albeit in a limited form. Additionally, the remarks relating to the authority of the OECD Commentary are thoroughly misplaced especially considering the plethora of judgments which have placed reliance on the OECD Commentary and laid importance on the OECD Commentary in interpreting provisions of tax treaties. With conflicting rulings being

delivered various Tribunals on the same issue, the uncertainty caused on this

particular subject is going to cause immense discomfort to foreign investors

dealing with

______________________ 1 (2005) 95 ITD 269 2 (2004) 192 CTR 257 (Supreme Court) 3 The Tribunal distinguished the Motorola case on the ground that the fact circumstances were different, as the software was provided as a package with the hardware and was to be utilized solely with such hardware. Further, the Tribunal did not place reliance upon the Tata Consultancy case as Supreme Court had delivered the judgment in the context of sales tax and not income tax. 4 The Tribunal placed reliance upon the Supreme Court ruling is CIT v P.V.A.L Kulandagam Chettiar (2004) 267 ITR 654 (SC) in this regard. 5 ADIT v M/s Solid Works Corporation AIT-2010-160-ITAT 6

Velankani Mauritius v. DDIT MANU/IL/0027/2010 7

ITA No.7349/Mum/2004 -

Ankita

Srivastava & Neha Sinha You may direct your comments to Ramya Krishnan-Anil +91 900465 0363

|

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|

|

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|

|

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||