|

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

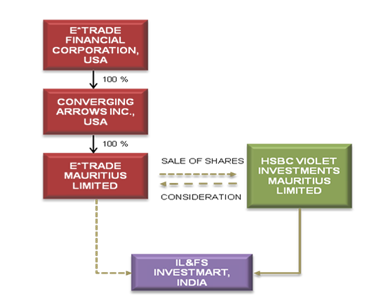

March 24, 2010 A Happy End to the E*Trade Mauritius Saga In a happy ending to the latest Mauritius saga in the case of E*Trade, the Authority for Advance Rulings (“AAR”) has ruled that E*Trade is entitled to the beneficial capital gains tax treatment under the India-Mauritius tax treaty (“Treaty”) and is hence not taxable in India. When the Indian tax authorities tried to deny tax treaty benefits to Mauritius based, E*Trade Mauritius Ltd., we ran two hotlines, E*Trade and the Mauritius route: Much ado about nothing? and E*Trade Mauritius Uproar - Tax Department’s Findings (An Update). The tax department’s approach, though flawed, was a cause of much commotion and anxiety among the global investing community. From the start, however, it seemed quite absurd to us that the revenue authorities were indirectly sitting on the judgment of the Indian Supreme Court in Azadi Bachao Andolan1 which upheld the validity of the Mauritius route and continues to be the law of the land. Finally, the AAR has followed the Azadi Bachao Andolan case and ruled that the benefits of the Treaty should be given to E*Trade. Truly, there has been much ado about nothing and we hope that this judgment provides the much needed relief to foreign investors. A Little Bit of History E*Trade Mauritius Ltd. (“ETM”) is a wholly owned subsidiary of US based Converging Arrows Inc (“CAI”), which is in turn a wholly owned subsidiary of E*Trade Financial Corporation (“ETFC”), also a US company. ETM was holding shares of an Indian company, IL&FS Investmart (“IL&FS”). The transaction in question was the sale of the entire stake of ETM in IL&FS to HSBC Violet Investments (“HSBC”), also based in Mauritius.

ETM received the funds for this transaction from CAI, its parent company. Taking benefit of the capital gains tax benefit under the Treaty, ETM sought a certificate from the Indian tax authorities (“Revenue”), authorizing payment of consideration by HSBC sans any withholding tax. Surprisingly, the Revenue refused to grant a nil withholding tax certificate. In this connection ETM filed a writ petition before the Bombay High Court, wherein the High Court without examining the merits of the case directed ETM to file a revision application before the Revenue. After the Bombay High Court’s order ETM approached the AAR to determine the Indian tax implications of sale of an Indian company’s shares by a Mauritius company and the applicability of Treaty benefits. The Revenue claimed that though the legal ownership of the shares in IL&FS resides with ETM, the real and beneficial owner of the capital gains is ETFC, and ETM is merely a facade developed to avoid tax on capital gains in India. To support this contention, the Revenue also stated that the transaction was funded indirectly by the ultimate parent company, ETFC. Last but not the least, the Revenue also argued that since the beneficial ownership of the IL&FS shares was with ETFC, the India-US Tax Treaty should be applied instead of the India-Mauritius Tax Treaty. Decision All along the ruling, it can be seen that the AAR has heavily relied on the Supreme Court’s decision2 in the landmark case of Azadi Bachao Andolan, which put an end to the debate relating to use of the beneficial treatment under the Treaty, by justifying treaty shopping. The AAR reiterated the Supreme Court’s decision and stated that the motive of tax avoidance was not relevant so long as the same was within the framework of law. It held that ‘Treaty Shopping’ was not against law and the corporate veil cannot be lifted to deny treaty benefits. The AAR also stated that since ETM was recognized as a shareholder of IL&FS and also received dividends in its capacity as a shareholder, merely because the transaction may have been indirectly funded by ETFC cannot lead to an inference that ETFC owned the shares in IL&FS. To take such a view would blur the mutual business and economic relations between a holding and subsidiary company. An important point made by the AAR is also that a subsidiary has its own corporate personality and the fact that ETFC exercises acts of control over ETM does not in the absence of compelling reasons dilute ETM’s separate legal identity. Lastly, on the argument with respect to beneficial ownership, the AAR held that the concept of ‘beneficial ownership’ which is used in the Treaty in connection with Interest and Dividend was irrelevant in the context of taxability of Capital Gains. Again, relying on Azadi Bachao Andolan and Circular No. 7893 and 6824 of the Central Board of Direct Taxes (“CBDT”), it concluded that a certificate of residence issued by the Mauritian authorities will constitute sufficient evidence for accepting the status of residence as well as beneficial ownership of shares. Further the Revenue also alleged that ETFC had ownership rights over IL&FS, as some directors were found to be common between ETFC and IL&FS. However, the AAR observed that the executive control over IL&FS was never exercised by the common directors and ETM’s status as a shareholder of IL&FS is not in any way affected by the overall control exercised by the US parent company. Our Analysis The E*Trade case had created a lot of uncertainty amidst foreign investors and private equity firms with respect to their investments made from Mauritius. Following this case, with a view to avoid litigation, some of the parties in private equity investment transactions preferred to make payments after deducting tax at source even though it was exempt from tax in the first instance. The Revenue’s attempt to introduce the concept of beneficial ownership in the context of taxability of capital gains is novel to Indian jurisprudence. In most treaties, reference to ‘beneficial ownership’ is used in connection with interest, dividends, royalties and fees for technical services. However, as regards capital gains, as rightly pointed by the AAR, the concept of beneficial ownership has no relevance. In fact, the AAR had recently held in KSPG Netherlands Holdings BV5 that while the concept of ‘beneficial ownership’ has no relevance in case of capital gains, even if it did apply, to the extent the intermediary has a distinct corporate personality with an independent board of directors and management systems, the intermediary cannot be considered as a sham entity deliberately set up to avoid capital gains tax liability. Further, although the AAR has not really gone into the cases where the corporate veil can be lifted, it is now a settled law that the corporate veil can be lifted only in cases of fraud or sham transactions where tax is sought to be evaded. With this ruling coupled with the legendary Azadi Bachao Andolan case, there seems to remain no doubt that capital gains tax benefits under the Treaty will be available to a tax resident of Mauritius. While this ruling definitely gives a breather to foreign investors, an interesting point that the AAR has discussed is the anomaly circling the fact that even though an Indian capital asset is being transferred, Indian tax authorities are not in a position to levy capital gains tax because of the inevitable effect of the Treaty read along with the circulars issued by CBDT and the law laid down in Azadi Bachao Andolan case. The AAR has also stated its inability to comment on whether the present day fiscal scenario requires policy considerations underlying this crucial Treaty. This still leaves us with an open question as to whether the Treaty will be re-negotiated and whether concepts such as the later in time doctrine in the Draft Direct Taxes Code are an effort by the Government to curb ‘Treaty Shopping’.

______________ 1 263 ITR 706. 2 Article 141 of the Constitution of India provides that the law declared by the Supreme Court of India shall be binding on all courts within the territory of India and shall be declared to be the law of the land. 3 Circular No. 789 dated April 13, 2000 clarifies that capital gains derived by a Mauritius resident from the sale of shares of an Indian company, in accordance with the Treaty are taxable only in Mauritius. The circular further indicates that a certificate of residence issued by the Mauritian tax authorities would constitute sufficient evidence for accepting the status of residence as well as beneficial ownership for applying the treaty. 4 Circular No. 682 dated March 30, 1994 provides that in terms of the Treaty, capital gains derived by a resident of Mauritius by alienation of shares of companies shall be taxable only in Mauritius according to Mauritius tax law. Therefore, any resident of Mauritius deriving income from alienation of shares of Indian companies will be liable to capital gains tax only in Mauritius as per the Mauritius tax law and will not have any capital gains tax liability in India.

Shreyas Jhaveri, Radhika Iyer & Parul Jain

You may direct your comments to Ramya Krishnan-AniL +91 900465 0363 |

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|

|

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||