|

December 6, 2008

The Vodafone Judgment: Tax Uncertainty for M&A and PE

Deals

One of the most anticipated judgments in recent times, the Order

of the Bombay High Court (“Court”)

in the Vodafone controversy, is finally out. This judgment

raises uncertainties with respect to taxation of cross-border

mergers and acquisitions between two foreign entities, involving

direct or indirect subsidiaries or affiliates in India. It also

brings uncertainty to private equity funds which acquire shares

of foreign companies in a similar fashion.

We had published our detailed commentaries on the Vodafone

Controversy as it had unfolded in the courtroom and we do not

wish to spill more ink recounting the arguments, which are

available at the footnote.*

The broad facts of the case are briefly summarized as follows:

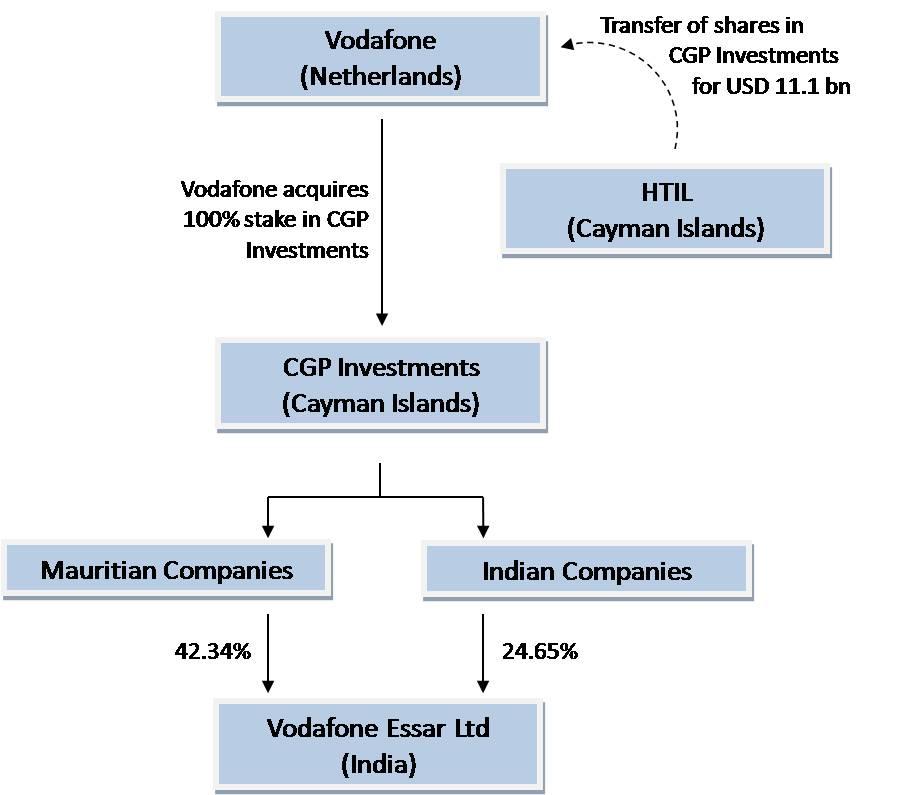

Shares of CGP Investments, a company incorporated in the Cayman

Islands were transferred by HTIL, another Cayman Islands company

to Vodafone International Holdings BV (“Vodafone”)

for a consideration of about USD 11.1 billion. CGP Investments

held stake in a series of Mauritian and Indian Companies which

cumulatively held about 67% stake in Vodafone Essar Limited (“VEL”).

The Indian Revenue Authorities (“Revenue”)

issued show cause notices (“Notices”)

to both Vodafone and VEL as to why they should not be held as

“assesses in default”, the former on the ground of failure to

withhold taxes at source and the latter as a “representative

assessee”. Both VEL and Vodafone filed respective writ petitions

before the Court challenging the validity of these Notices

The Court has dismissed Vodafone’s writ petition on the ground

of non-maintainability. As we had reported on December 3, 2008,

the Court has dismissed the writ petition and has made five

important observations. In today’s commentary, we have analyzed

these observations and have also set out our analysis of the

judgment. The five observations made by the Court before

dismissing the petition are:

-

Vodafone had approached the Foreign Investment Promotion

Board (“FIPB”)

before effecting the transfer of shares of the Cayman

Islands entity. Therefore it was within the jurisdiction of

the Revenue to proceed against Vodafone and the Notice

served was valid;

-

The transaction amounted to an indirect transfer of

controlling interest in VEL, an Indian company and hence an

indirect transfer of capital asset situated in India;

-

The transaction created a “real link” between India and

Vodafone, so as to bring the consideration to tax in line

with the “Effects Doctrine” as understood in USA;

-

The agreement entered into between Vodafone and the vendor

was not furnished before the revenue authorities or the

Court;

-

The writ petition to impugn the Notice was not maintainable

when an alternative statutory remedy was available to

Vodafone

It must also be pointed out that while the Court made the above

observations, it has not held that Vodafone is liable to pay tax

or penalties under the ITA.

It is pertinent to note that the Vodafone controversy is not

limited to the writ petition filed by Vodafone but also the writ

petition filed by VEL. However, the order seems to dismiss the

entire controversy solely on the submissions made by Vodafone

without hearing the submissions of VEL. With due respect, this

seems to be in the teeth of the principles of natural justice

which require a party to be heard before any judgment is passed.

While the writ petition has been dismissed by the Court, the

issues relating to the Vodafone controversy have not been

settled and the Order leaves much to be desired.

________________________________

* We had published our daily commentaries on

the Vodafone Controversy as it had unfolded in the courtroom.

These commentaries can be accessed here:

June 27, 2008,

June 30, 2008

July 2, 2008,

July 8, 2008, July

9, 2008,

July 10, 2008,

December 3, 2008

|

|

|

You can

direct your queries or comments to the authors

|

|