|

|

|

|

|

|

|

June 17, 2009

Tax Authorities Shed Light On Taxation Of Composite Contracts Having

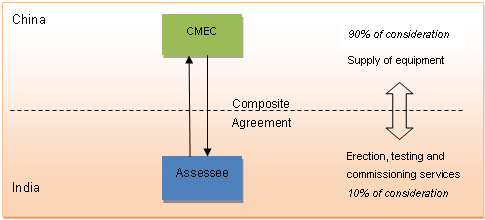

Separate Identifiable Segments In a case involving a composite contract between entities in India and China, the Income Tax Appellate Tribunal, Hyderabad Bench (“ITAT”) in Andhra Pradesh Power Generation Corporation Ltd.,1 held that if there are two separate identifiable segments of the composite contract, only income arising from that part of the composite contract under which services are provided in India is subject to tax in India. Facts Andhra Pradesh Power Generation Corporation Ltd. (“Assessee”)

entered into an agreement with National Machinery And Equipment Import

And Export Corporation

The AO observed that CMEC continued to exercise

control over the equipment which resulted in CMEC having a business

connection in Judgment The ITAT agreed with AO’s primary finding that it

was one composite contract which has been split into two separate

identifiable contracts, one relating to supply of equipment which had

taken place outside India and the other one relating to erection,

testing and other related services which took place in India. As regards

the contention regarding the PE in India, it is pertinent to note that

the Double Taxation Avoidance Agreement between India and China spells

out under Article 7(1) that no business profit would arise in India if

an enterprise proves that the business activities have no relation with

the permanent establishment in India. Since the equipments were not

manufactured in ITAT also observed that if parties have contracted

that it is a free on board (FOB) contract and title in the goods shall

pass outside Analysis Surprisingly, the ITAT in this judgment has not

made a reference to the landmark Ishikawajma case although it is substantially in consonance with the

principle followed by the Supreme Court in that case.

Ishikawajma2 which had similar facts as the present case ruled that

only such part of the income in a composite contract as is attributable

to operations carried out in The Worley Parsons Ruling3 which created some concerns a few months back,

questioned the very basis of the doctrine of territorial nexus which had

been laid down by the Supreme Court in its ruling of

Ishikawajma and developed by the recent ruling of

Clifford

Chance4. However, considering the facts of this case,

it may not be possible to compare this judgment with the

Worley Parsons Ruling as unlike the facts involved in

Worley Parsons, the supply of equipment which forms 90% of the

contract consideration is not a pre-requisite for the services provided

under the contract in ____________________________

3 Advance ruling given in WorleyParsons Services Pty. Ltd. dated March 30, 2009 discusses in detail the judgment given in Ishikawajma. The ruling given in this case is a diversion from the judgment of Supreme Court in the Ishikawajma. However, it is pertinent to note here that this is an advance ruling and is specific to the facts of that particular case. It does not hold any binding effect on the courts although it may have a limited amount of persuasive value.

|

|

|

| Disclaimer: The contents of this hotline should not be construed as legal opinion. View detailed disclaimer. |

This hotline provides general information existing at the time of preparation. The hotline is intended as a news update and Nishith Desai Associates neither assumes nor accepts any responsibility for any loss arising to any person acting or refraining from acting as a result of any material contained in this hotline. It is recommended that professional advice be taken based on the specific facts and circumstances. This hotline does not substitute the need to refer to the original pronouncements. This is not a Spam mail. You have received this mail because you have either requested for it or someone must have suggested your name. Since India has no anti-spamming law, we refer to the US directive, which states that a mail cannot be considered Spam if it contains the sender's contact information, which this mail does. In case this mail doesn't concern you, please unsubscribe from mailing list. |

| NDA |